How to Increase Your Business Line of Credit

Business lines of credit help you plug cash flow gaps, latch on to opportunities that need immediate investment, and grow your business on your terms.

Business lines of credit help you plug cash flow gaps, latch on to opportunities that need immediate investment, and grow your business on your terms.

Your business line of credit started at $25,000 two years ago. It was perfect then—enough cushion for seasonal dips, unexpected expenses, and the occasional opportunity.

But your business has grown. Revenue is up 40%, you’ve added employees, and that $25,000 credit line that once felt generous now feels tight. You regularly end up using 90% of your available credit, which means you’re one equipment failure or delayed client payment away from maxing out.

You need more credit capacity. The question is: can you—and how do you—get your lender to increase your line of credit?

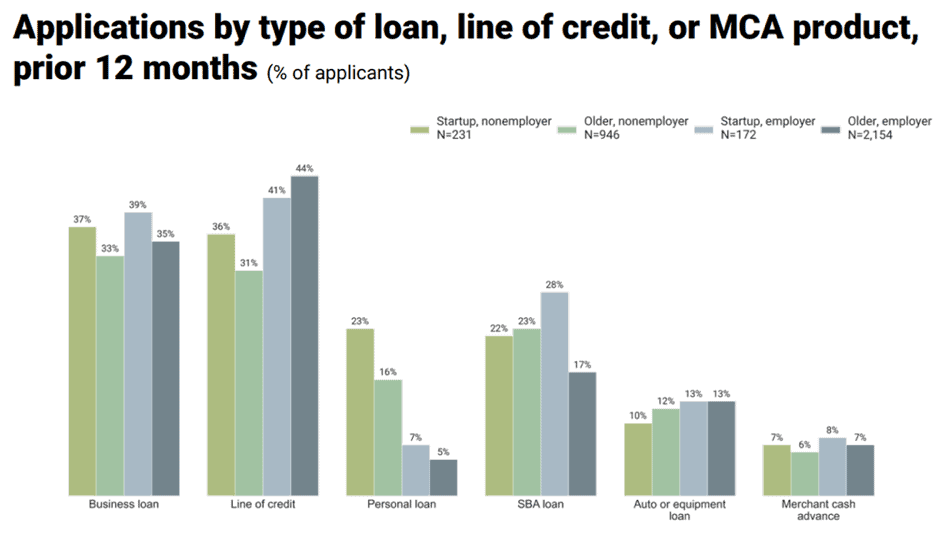

According to the 2024 Small Business Credit Survey by the Federal Reserve Banks, 40% of small businesses applied for business lines of credit—the highest rate of any credit type.

Image source: https://www.fedsmallbusiness.org/reports/survey/2024/2024-report-on-startup-firms

But not everyone who wants an increase gets approved. Business lines of credit typically range from $5,000 to $500,000, with some lenders offering limits up to $5 million for highly qualified businesses.

The good news? Increasing your business line of credit is entirely achievable if you understand what lenders look for, prepare the right documentation, and approach the request strategically.

Let’s break down exactly how to get your credit line increased—whether you’re seeking a modest bump or a significant expansion.

Before diving into how to increase your limit, understand why it matters:

Purchasing Power: A higher limit gives you more capacity to cover expenses, invest in opportunities, and handle seasonal cash flow swings without maxing out.

Credit Utilization Ratio: Keeping your utilization below 30% of your total credit limit signals responsible borrowing and improves your business credit score. If you’re consistently using 70-80% of your limit, you’re signaling potential cash flow stress to credit bureaus.

Financial Flexibility: Higher limits provide buffers for emergencies and build stronger supplier relationships without straining cash flow.

Better Terms: Businesses that manage higher credit limits responsibly often qualify for better rates and terms on future financing.

Small business credit card limits typically range from $10,000 to $50,000, while premium cards may exceed $100,000. For dedicated business lines of credit, limits vary even more widely based on business qualifications.

Before requesting an increase, understand how lenders determine credit limits:

Payment History: Your payment history is one of the most important factors lenders consider. If you have a history of paying bills on time and in full, you’re more likely to be approved for a credit line increase. Late payments or missed payments significantly hurt your chances.

Credit Utilization: Lenders analyze how much of your existing credit you’re using. Paradoxically, if you’re consistently maxing out your current line, lenders may view you as overextended rather than creditworthy. Aim to keep utilization below 30% before requesting increases.

Revenue and Cash Flow: Lenders look at your full financial picture, including your business’s assets, liabilities, current debt, and cash flow. According to research, banks analyze overall creditworthiness, collateral, and cash flow from operations when making credit decisions.

Business Credit Score: Your business credit score (from Dun & Bradstreet, Experian Business, or Equifax Business) significantly impacts approval decisions and the size of increase offered.

Personal Credit Score: For small businesses, personal credit scores typically matter more (and are often required). Wells Fargo, for example, typically requires guarantors to have FICO scores of at least 680 for their BusinessLine product.

Time in Business: Longer operating history demonstrates stability. Banks typically want 1-2+ years in business for credit increases, while some online lenders have more flexible criteria.

Financial Covenants Compliance: If your existing line of credit includes covenants (requirements around working capital, liquidity, debt coverage, owner compensation, or capital spending), you must be in compliance to qualify for increases.

Don’t request arbitrary amounts. Calculate your actual funding requirements using a twelve-month cash flow forecast that incorporates accurate projections for key cash flow sources.

The true purpose of a line of credit is filling funding gaps that occur due to cyclical business nature caused by increases in accounts receivable and inventory from increased sales—not purchasing long-term assets or funding losses.

Calculate your peak funding needs:

Example:

Remember: It’s important NOT to request more financing than you really need. If you ask for more than you need, the bank will question your competence—their confidence in you as a business owner is an important factor in their decision-making process.

Want to plug holes in your cash flow? Fight or recover from a lawsuit? Fulfil an order that seems beyond your reach?

Proper documentation significantly enhances your chances of approval. Gather these materials before requesting an increase:

Financial Statements

Provide statements for at least the last 12-24 months, ideally prepared by a CPA or using professional accounting software.

Bank Statements

Provide recent bank statements (typically 3-6 months) showing cash flow management and financial stability.

Tax Returns

Business tax returns for the past 2-3 years demonstrate consistent revenue and profitability trends.

Credit Reports

Obtain both business credit reports (from Dun & Bradstreet, Experian Business, Equifax Business) and personal credit reports. Review for accuracy and dispute any errors before submitting your request.

Business Plan and Projections

An updated business plan outlining your business model, market analysis, growth strategy, and financial projections demonstrates strategic vision and future profitability.

Details of Existing Credit

Include information about all existing credit lines, loans, and other financial obligations. This helps lenders understand your current debt situation and repayment capacity.

Before requesting an increase, take steps to improve your approval odds.

Improve your credit score:

Business Credit:

Personal Credit:

Reduce credit utilization:

If you’re using 70-80% of your current limit, pay down balances before requesting an increase. Asking for a credit line increase after keeping utilization low shows lenders you can manage credit responsibly.

Demonstrate revenue growth:

Lenders want to see a history of revenue growth, average monthly spend increases, and strong financial performance. Prepare documentation showing year-over-year revenue increases and positive trends.

Clean up your balance sheet:

Maintain perfect payment history:

Establish at least 6-12 months of perfect payment history on your existing line before requesting an increase. Establishing a positive repayment history with your existing lender proves you can manage higher limits.

Proactive communication with your banker is probably the most important yet understated factor—not just when trying to increase credit but all the time.

Don’t only talk to your banker when you need to borrow money. Maintain an ongoing relationship:

Don’t forget to share positive developments that demonstrate business growth:

Some lenders increase limits automatically based on account performance. They may increase your business credit card limit automatically if you demonstrate a strong payment history and business growth.

Many lenders conduct annual reviews that may result in limit increases, decreases, or closure based on performance and changing risk assessments.

Virtually every line of credit comes with financial covenants—conditions you must meet. Understand these covenants and comply with them. Common covenants include working capital minimums, liquidity requirements, and debt coverage ratios.

Always make your banker’s job easy by providing documentation proactively, on time.

It’s hard for lenders to trust you. But 75+ of the biggest ones trust us.

We can make our relationships work for YOU.

Once you’ve prepared thoroughly, it’s time to formally request the increase. What’s important here?

Your request should include:

Request increases when:

The approval process can take several weeks while lenders review your account, so plan accordingly.

Refused by multiple lenders? Badly need funds? Don’t fret.

If your current lender denies your request or offers an inadequate increase, explore alternative lending:

Work With Finance Brokers

This is where companies like QualiFi provide enormous value. Instead of being limited to one lender’s decision, brokers access networks of 75+ lenders with varying qualification criteria and credit limits.

The QualiFi advantage includes:

Apply for Additional Lines

You can maintain multiple lines of credit from different lenders simultaneously. If your current $25,000 line won’t increase, you might secure a separate $50,000 line from another lender.

Consider SBA CAPLines

For larger needs, SBA CAPLines provide revolving lines of credit for short-term working capital. According to SBA data, they’ve approved 104 CAPLines totaling over $103 million in fiscal year 2025. These programs can facilitate lines up to $5 million with longer maturities (up to 10 years).

Research Online Lenders

Fintech lenders often have more flexible criteria than traditional banks, though they typically charge higher rates. They may approve larger limits for businesses banks reject or offer inadequate increases to.

One application, multiple lenders lined up for you. Funding in 48 hours.

Start by reviewing the timeline. According to industry sources, the approval process typically takes several weeks. Lenders review:

The outcomes of your application may not necessarily be what you expected.

If approved,

If denied,

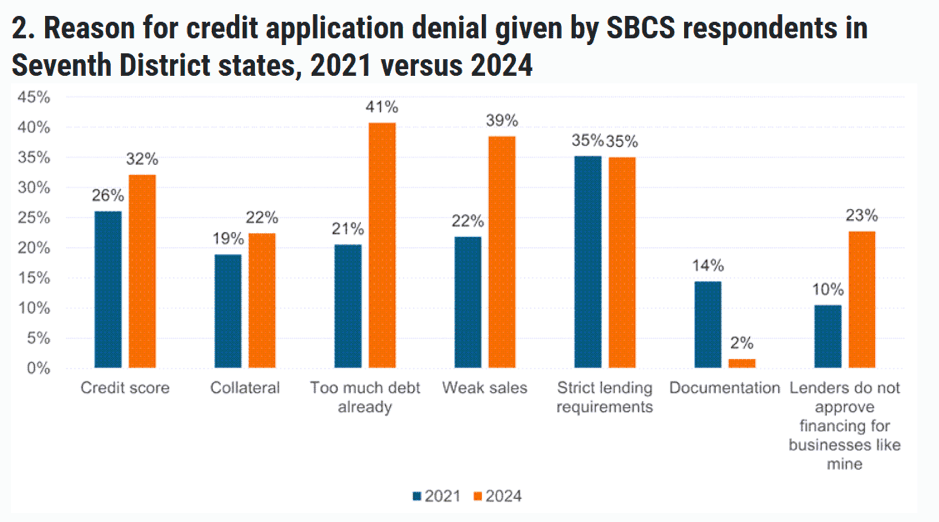

Image source: https://www.chicagofed.org/publications/chicago-fed-insights/2025/2024-small-business-credit-survey

Once approved, use your increased limit strategically.

Maintain Low Utilization

Even with a higher limit, keep utilization under 30%. If your limit increases from $25,000 to $75,000, use less than $22,500 regularly.

Continue Perfect Payments

Never become complacent. Late payments can trigger credit line reductions or closure.

Use the Credit Line for Appropriate Purposes

Lines of credit work best for:

Don’t use lines of credit for:

Monitor Covenant Compliance

Stay aware of all covenant requirements and monitor compliance monthly. Violations can trigger default even with perfect payments.

Watch Your Personal Credit Score

For lines requiring personal guarantees, increases may appear on personal credit reports. Factor this into timing if you’re planning major personal credit activities.

Increasing your business line of credit is achievable when you:

While typical business lines of credit range from $5,000 to $500,000, some lenders will offer up to $5 million for highly qualified businesses. The limit you qualify for depends on your business’s financial health, credit history, and growth trajectory.

Whether you’re seeking a modest increase to accommodate business growth or a substantial expansion to support major initiatives, the strategies outlined here will position you for success.

The businesses with the highest credit limits aren’t necessarily the largest—they’re the ones that consistently demonstrate financial responsibility, maintain strong lender relationships, and use credit strategically to support sustainable growth.

All the funding you need, when you need it, within the time you need it.

How long should I wait before requesting a credit line increase?

Wait at least 6-12 months after opening your line of credit before requesting an increase. During this time, establish perfect payment history, maintain credit utilization below 30%, and demonstrate business growth. The longer your positive track record, the better your approval odds and potential increase amount.

Will requesting a credit line increase hurt my credit score?

It depends. Some lenders perform soft inquiries that don’t affect credit scores, while others require hard inquiries that may temporarily lower scores by a few points. Ask your lender which type they’ll use before requesting. However, if approved, the higher limit can actually improve your credit score by lowering your credit utilization ratio—assuming your spending remains constant.

What credit score do I need for a line of credit increase?

Requirements vary by lender. Traditional banks typically require personal FICO scores of at least 680. Business credit scores should generally be in the “good” range (75+ on the PAYDEX scale, 75+ on Experian Business scale). However, finance brokerage firms such as QualiFi can match you with lenders whose criteria align with your credit profile and may approve increases with lower scores.

Can I have multiple business lines of credit simultaneously?

Yes. There’s no restriction on maintaining lines of credit from different lenders. In fact, having multiple lines can be strategic—diversifying credit sources and providing larger total capacity. However, each line requires separate applications, may require personal guarantees, and contributes to your total debt obligations. Ensure you can manage payments on all lines and that multiple guarantees don’t overextend your personal credit.

What’s the maximum business line of credit I can get?

Limits vary dramatically. Small business credit cards typically range from $10,000 to $100,000+. Traditional business lines range from $5,000 to $500,000, with some lenders offering up to $5 million. Your maximum depends on revenue, credit scores, time in business, financial health, collateral (for secured lines), and lender policies.

What happens if my request to increase my line of credit is denied?

Request specific denial reasons from your lender. Common issues include insufficient time in business, low credit scores, high existing debt, negative payment history, and declining revenues. Address the specific issues raised while you wait out the 6-12 months before you can reapply. Alternatively, work with finance brokers like QualiFi who have simultaneous access to multiple lenders.

Should I increase my line of credit or apply for a new one?

Increasing existing lines is usually preferable—it involves simpler processes, one relationship to manage, and potentially better terms due to existing arrangements.. However, you should apply for new lines when you need more capacity than one lender will provide, your current lender denies an increase, or other lenders offer significantly better terms.

https://goqualifi.com/wp-content/uploads/2023/01/Image-of-money-laying-ontop-of-a-camouflage-uniform..jpg

1250

2000

Gia

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

Gia2026-02-26 02:39:282026-02-27 02:41:5412 Liquidity Strategies That Keep Your Business Going Always

https://goqualifi.com/wp-content/uploads/2023/01/Image-of-money-laying-ontop-of-a-camouflage-uniform..jpg

1250

2000

Gia

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

Gia2026-02-26 02:39:282026-02-27 02:41:5412 Liquidity Strategies That Keep Your Business Going Always https://goqualifi.com/wp-content/uploads/2026/02/entrepreneur_quotes.jpg

848

1280

Gia

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

Gia2026-02-19 05:38:392026-02-19 05:38:4250 Quotes from Top Business Leaders—And What They Really Mean!

https://goqualifi.com/wp-content/uploads/2026/02/entrepreneur_quotes.jpg

848

1280

Gia

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

Gia2026-02-19 05:38:392026-02-19 05:38:4250 Quotes from Top Business Leaders—And What They Really Mean! https://goqualifi.com/wp-content/uploads/2025/11/debt.png

522

939

Gia

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

Gia2026-02-13 04:37:522026-02-13 04:39:51What Is the Cost of Debt? (And How to Calculate It)

https://goqualifi.com/wp-content/uploads/2025/11/debt.png

522

939

Gia

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

Gia2026-02-13 04:37:522026-02-13 04:39:51What Is the Cost of Debt? (And How to Calculate It) https://goqualifi.com/wp-content/uploads/2025/10/line-of-credit.png

608

939

Gia

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

Gia2026-02-05 07:39:292026-02-05 07:41:31How to Increase Your Business Line of Credit

https://goqualifi.com/wp-content/uploads/2025/10/line-of-credit.png

608

939

Gia

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

Gia2026-02-05 07:39:292026-02-05 07:41:31How to Increase Your Business Line of Credit https://goqualifi.com/wp-content/uploads/2026/01/emergency_funding.jpg

698

1280

Gia

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

Gia2026-01-30 08:00:292026-01-30 08:19:33What to Do When You Need Emergency Business Funding

https://goqualifi.com/wp-content/uploads/2026/01/emergency_funding.jpg

698

1280

Gia

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

Gia2026-01-30 08:00:292026-01-30 08:19:33What to Do When You Need Emergency Business Funding https://goqualifi.com/wp-content/uploads/2026/01/business-momentum.jpg

640

1280

Gia

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

Gia2026-01-23 13:26:172026-02-13 04:54:55Does Your Business Have Momentum? These 10 Parameters Will Tell You

https://goqualifi.com/wp-content/uploads/2026/01/business-momentum.jpg

640

1280

Gia

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

Gia2026-01-23 13:26:172026-02-13 04:54:55Does Your Business Have Momentum? These 10 Parameters Will Tell You https://goqualifi.com/wp-content/uploads/2023/01/Image-of-a-business-person-loaning-money..jpg

1250

2000

Gia

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

Gia2026-01-19 07:38:012026-01-30 08:19:32Merchant Cash Advance (MCA) Loans: A Strategic Guide for Small Businesses

https://goqualifi.com/wp-content/uploads/2023/01/Image-of-a-business-person-loaning-money..jpg

1250

2000

Gia

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

Gia2026-01-19 07:38:012026-01-30 08:19:32Merchant Cash Advance (MCA) Loans: A Strategic Guide for Small Businesses https://goqualifi.com/wp-content/uploads/2023/06/Buesiness-people-signing-paperwork.jpg

1250

2000

Gia

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

Gia2026-01-09 07:49:072026-01-30 03:21:28How to Find the Best Finance Brokerage Firm

https://goqualifi.com/wp-content/uploads/2023/06/Buesiness-people-signing-paperwork.jpg

1250

2000

Gia

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

Gia2026-01-09 07:49:072026-01-30 03:21:28How to Find the Best Finance Brokerage Firm https://goqualifi.com/wp-content/uploads/2025/04/Team-Putting-Hands-in-a-Circle.jpg

844

2000

Gia

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

Gia2025-12-30 07:59:312025-12-30 07:59:35How to Organize Your Business Finances Smartly

https://goqualifi.com/wp-content/uploads/2025/04/Team-Putting-Hands-in-a-Circle.jpg

844

2000

Gia

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

Gia2025-12-30 07:59:312025-12-30 07:59:35How to Organize Your Business Finances Smartly