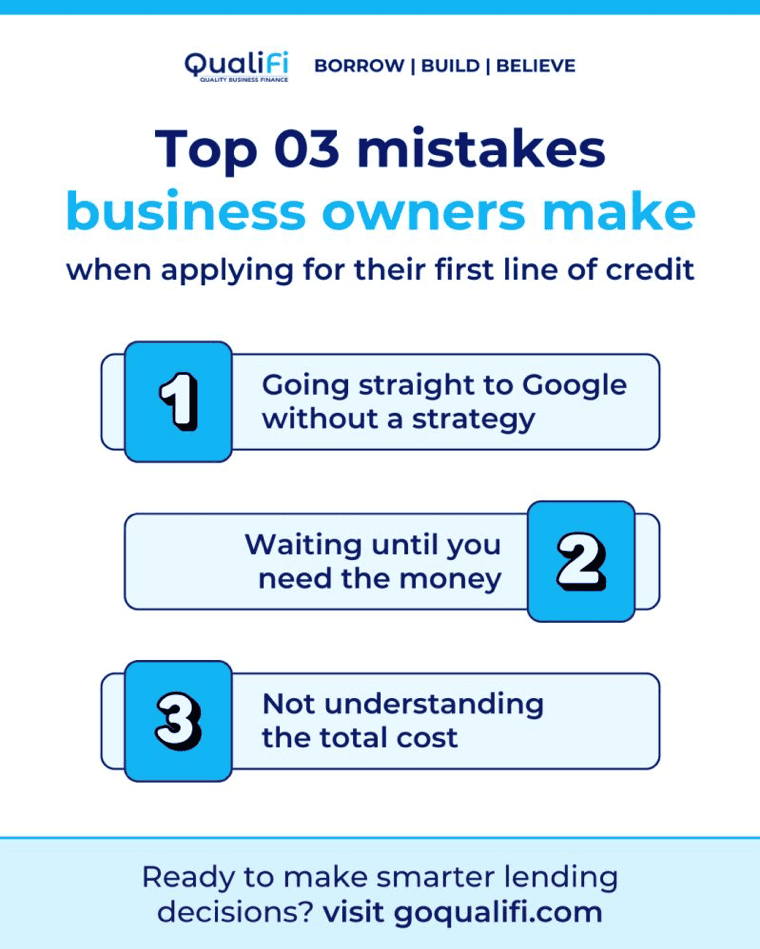

The 3 Biggest Mistakes Business Owners Make When Applying for Their First Line of Credit

Don’t go in blind. Don’t wait till your cash runs out. Don’t ignore the total cost you pay.

Don’t go in blind. Don’t wait till your cash runs out. Don’t ignore the total cost you pay.

Getting your first line of credit is one of those business milestones you’ll always remember. It’s often the first time you feel like your business has crossed into “real player” territory-where you’ve proven enough to get external backing and can finally access the capital to take things to the next level.

Done right, a line of credit gives you flexibility: the freedom to smooth out seasonal dips, the ability to seize time-sensitive opportunities, and the confidence to invest in growth without draining your cash reserves.

Done wrong? It can do the opposite. You might get stuck with terms that eat into your profits, end up paying way more than you expected, or worse, find yourself rejected entirely right when you need funding most.

The truth is, we’ve helped secure hundreds of millions in funding for small businesses, and the same missteps show up time and time again. The good news is they’re not set in stone. With the right approach, you can sidestep them and put your business in the best position for success.

Here are the three biggest mistakes business owners make when applying for their first line of credit-and how you can avoid them.

When most business owners decide they need financing, they follow the same instinct: open up Google, type “business loan,” and click whatever pops up first.

It makes sense. After all, that’s how we find everything else these days, from restaurants and mechanics to vacation rentals. Financing isn’t the same as booking a hotel. By relying on the first lender you find, you’re essentially putting all your eggs in one basket.

Why’s that a problem? Because no two lenders look at your potential the same way.

Read our guide on how limiting yourself to one lender or bank can hold your business back.

There are over 70 different lenders in the marketplace, each with its own risk tolerance, industry preferences, and underwriting criteria.

Some specialize in startups. Others avoid them completely.

Some are all about collateral. Others prefer recurring revenue.

Some only work with businesses in certain sectors.

If your profile doesn’t line up perfectly with their box, you’ll either get rejected or be offered terms that aren’t in your favor.

So, what do we suggest? Don’t just click the first link that appears. Work with someone who understands the landscape. A good broker has relationships with dozens of lenders and knows how to match your specific situation to the right fit. That means more options, better rates, and a faster process, without you wasting hours filling out applications that go nowhere.

This is the number one trap we see: business owners waiting until the pressure is on to apply for a loan.

Cash is already tight, sales are down, and suddenly there’s a payroll gap or an opportunity that requires capital. That’s when they reach out. The problem? Lenders don’t like lending to businesses that look like they’re in trouble.

When your bank statements show declining balances or irregular deposits, your options shrink-and the offers you do get often come with higher interest rates, stricter terms, and lower limits. In other words, the exact opposite of what you actually need in that moment.

It may seem counterintuitive, but the reality is straightforward: the best time to apply is when you don’t need the money. When your financials are strong, your approval odds go up, your cost of capital goes down, and you can lock in flexible structures that actually support growth.

You don’t buy health insurance when you’re already in the hospital-you buy it when you’re healthy so it’s there when things get bumpy. The same goes for business credit. Secure it in advance, so when you do need it, it’s ready to go.

Here’s a mistake we see far too often: focusing only on the payment.

On the surface, a “low monthly payment” might look like a win. But financing isn’t just about what leaves your account every 30 days-it’s about the total cost of capital. That includes:

When you add it all up, what seemed like an affordable deal can actually end up costing you double what you expected.

Instead, always ask your broker or lender to walk you through the total cost, not just the installment. Compare options based on the full picture, not just the monthly bite. And above all, read the fine print before signing. A little diligence up front can save you tens of thousands over the life of the credit line.

QualiFi eliminates the hurdles imposed by regular banks. We can get you funding within days, rather than weeks, with minimal documentation.

Your first line of credit can either be a launchpad or a stumbling block. Avoiding these three mistakes-going in blind, waiting until it’s too late, and overlooking the true cost-will set you up to secure financing that’s not just accessible, but actually works in your favor.

At QualiFi, we’ve built our entire model around helping business owners avoid these pitfalls. We know the lenders. We understand the underwriting. And we know how to tell your story in a way that gets results. That’s why we’ve helped secure over $500 million in funding for businesses like yours.

Here’s why businesses of all sizes TRUST US over other banks, lenders and brokers!

If you’re considering your first line of credit, don’t settle for guesswork or cookie-cutter answers. A quick discovery call with our team could be the difference between settling for “just enough” and unlocking financing that truly fuels your growth.

GIVE US A CALL ON 833.933.3665

OR

https://goqualifi.com/wp-content/uploads/2026/03/Restaurant-Financing-101-From-Food-Trucks-to-Fine-Dining.webp

341

512

faras@brandmaximise.com

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

faras@brandmaximise.com2026-03-23 23:16:292026-03-23 23:16:31Restaurant Financing 101: From Food Trucks to Fine Dining – Complete guide to funding options for every stage of restaurant growth

https://goqualifi.com/wp-content/uploads/2026/03/Restaurant-Financing-101-From-Food-Trucks-to-Fine-Dining.webp

341

512

faras@brandmaximise.com

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

faras@brandmaximise.com2026-03-23 23:16:292026-03-23 23:16:31Restaurant Financing 101: From Food Trucks to Fine Dining – Complete guide to funding options for every stage of restaurant growth https://goqualifi.com/wp-content/uploads/2026/03/What-13-Years-in-Alternative-Lending-Taught-Us-About-Small-Business.webp

393

650

faras@brandmaximise.com

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

faras@brandmaximise.com2026-03-23 23:07:192026-03-23 23:07:21What 13 Years in Alternative Lending Taught Us About Small Business

https://goqualifi.com/wp-content/uploads/2026/03/What-13-Years-in-Alternative-Lending-Taught-Us-About-Small-Business.webp

393

650

faras@brandmaximise.com

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

faras@brandmaximise.com2026-03-23 23:07:192026-03-23 23:07:21What 13 Years in Alternative Lending Taught Us About Small Business https://goqualifi.com/wp-content/uploads/2026/03/Your-Businesss-Financial-Health-Check-10-Key-Metrics-That-Actually-Matter.png

382

680

faras@brandmaximise.com

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

faras@brandmaximise.com2026-03-21 23:26:382026-03-21 23:26:41Your Business’s Financial Health Check: 10 Key Metrics That Actually Matter

https://goqualifi.com/wp-content/uploads/2026/03/Your-Businesss-Financial-Health-Check-10-Key-Metrics-That-Actually-Matter.png

382

680

faras@brandmaximise.com

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

faras@brandmaximise.com2026-03-21 23:26:382026-03-21 23:26:41Your Business’s Financial Health Check: 10 Key Metrics That Actually Matter https://goqualifi.com/wp-content/uploads/2026/03/Beyond-Banks-Why-Alternative-Lending-Might-Be-Your-Best-Option.jpg

382

706

faras@brandmaximise.com

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

faras@brandmaximise.com2026-03-21 23:15:482026-03-21 23:28:36Beyond Banks: Why Alternative Lending Might Be Your Best Option

https://goqualifi.com/wp-content/uploads/2026/03/Beyond-Banks-Why-Alternative-Lending-Might-Be-Your-Best-Option.jpg

382

706

faras@brandmaximise.com

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

faras@brandmaximise.com2026-03-21 23:15:482026-03-21 23:28:36Beyond Banks: Why Alternative Lending Might Be Your Best Option https://goqualifi.com/wp-content/uploads/2026/03/Labor-Market-Tight-How-to-Finance-Employee-Retention-and-Recruitment.png

449

800

faras@brandmaximise.com

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

faras@brandmaximise.com2026-03-19 14:00:002026-03-19 11:47:15Labor Market Tight? How to Finance Employee Retention and Recruitment

https://goqualifi.com/wp-content/uploads/2026/03/Labor-Market-Tight-How-to-Finance-Employee-Retention-and-Recruitment.png

449

800

faras@brandmaximise.com

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

faras@brandmaximise.com2026-03-19 14:00:002026-03-19 11:47:15Labor Market Tight? How to Finance Employee Retention and Recruitment https://goqualifi.com/wp-content/uploads/2026/03/Emergency-Business-Funding-When-You-Need-Capital-Now-Fast-funding-options-for-urgent-needs.jpg

551

1000

faras@brandmaximise.com

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

faras@brandmaximise.com2026-03-19 11:37:112026-03-19 11:37:14Emergency Business Funding: When You Need Capital Now – Fast funding options for urgent needs

https://goqualifi.com/wp-content/uploads/2026/03/Emergency-Business-Funding-When-You-Need-Capital-Now-Fast-funding-options-for-urgent-needs.jpg

551

1000

faras@brandmaximise.com

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

faras@brandmaximise.com2026-03-19 11:37:112026-03-19 11:37:14Emergency Business Funding: When You Need Capital Now – Fast funding options for urgent needs https://goqualifi.com/wp-content/uploads/2026/03/How-to-Inflation-Proof-Your-Business-Financial-Strategies-for-Uncertain-Times.webp

1080

1920

faras@brandmaximise.com

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

faras@brandmaximise.com2026-03-18 13:30:002026-03-18 11:19:16How to Inflation-Proof Your Business: Financial Strategies for Uncertain Times

https://goqualifi.com/wp-content/uploads/2026/03/How-to-Inflation-Proof-Your-Business-Financial-Strategies-for-Uncertain-Times.webp

1080

1920

faras@brandmaximise.com

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

faras@brandmaximise.com2026-03-18 13:30:002026-03-18 11:19:16How to Inflation-Proof Your Business: Financial Strategies for Uncertain Times https://goqualifi.com/wp-content/uploads/2026/03/Understanding-the-Effects-of-Fed-Rate-Hikes-on-Small-Business-Financing-1.webp

775

1200

faras@brandmaximise.com

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

faras@brandmaximise.com2026-03-18 11:05:302026-03-18 11:05:33Understanding the Effects of Fed Rate Hikes on Small Business Financing

https://goqualifi.com/wp-content/uploads/2026/03/Understanding-the-Effects-of-Fed-Rate-Hikes-on-Small-Business-Financing-1.webp

775

1200

faras@brandmaximise.com

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

faras@brandmaximise.com2026-03-18 11:05:302026-03-18 11:05:33Understanding the Effects of Fed Rate Hikes on Small Business Financing https://goqualifi.com/wp-content/uploads/2026/03/From-500K-to-5M-Scaling-Your-Construction-Business-the-Right-Way-1.webp

647

1379

faras@brandmaximise.com

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

faras@brandmaximise.com2026-03-17 13:00:002026-03-17 13:50:39From $500K to $5M: Scaling Your Construction Business the Right Way

https://goqualifi.com/wp-content/uploads/2026/03/From-500K-to-5M-Scaling-Your-Construction-Business-the-Right-Way-1.webp

647

1379

faras@brandmaximise.com

https://goqualifi.com/wp-content/uploads/2024/01/qualifi-new-logo-300x106.jpg

faras@brandmaximise.com2026-03-17 13:00:002026-03-17 13:50:39From $500K to $5M: Scaling Your Construction Business the Right Way